People of any age with End-Stage Renal Disease (ESRD)

The Different Parts of Medicare

The different parts of Medicare help cover specific services:

Medicare Part A (Hospital Insurance)

Helps cover inpatient care in hospitals

Helps cover skilled nursing facility, hospice, and home health care

Medicare Part B (Medical Insurance)

Helps cover doctors’ services, hospital outpatient care, and home health care

Helps cover many preventive services to help maintain your health and to keep certain illnesses from getting worse

Medicare Part D (Medicare Prescription Drug Coverage)

A prescription drug option run by Medicare-approved private insurance companies

Helps cover the cost of prescription drugs

May help lower your prescription drug costs and help protect against higher costs in the future

Enrolling in Medicare

Signing Up for Part A and Part B Automatically:

In most cases, if you’re already getting benefits from Social Security or the Railroad Retirement Board (RRB), you will automatically get Part A and Part B starting the first day of the month you turn 65. If your birthday is on the first day of the month, Part A and Part B will start the first day of the prior month. You will get your red, white, and blue Medicare card in the mail 3 months before your 65th birthday or your 25th month of disability. If you don’t want Part B, follow the instructions that come with the card, and send the card back. If you keep the card, you keep Part B and will pay Part B premiums.

How to Sign up for Part A and Part B

Call Social Security at 1-800-772-1213 for more information about your Medicare eligibility, and to sign up for Part A and/or Part B. If you’re 65 or older, you can also apply for premium-free Part A and Part B online at www.socialsecurity.gov/retirement. The whole process can take less than 10 minutes.

When Can You Sign Up For Medicare?

Initial Enrollment Period

You can sign up when you’re first eligible for Part B. (For example, if you’re eligible for Part B when you turn 65, this is a 7-month period that begins 3 months before the month you turn 65, includes the month you turn 65, and ends 3 months after the month you turn 65.)

General Enrollment Period

If you didn’t sign up for Part A and/or Part B (for which you pay monthly premiums) when you were first eligible, you can sign up between January 1–March 31 each year. Your coverage will begin July 1. You may have to pay a higher premium for late enrollment.

Special Enrollment Period

If you didn’t sign up for Part A and/or Part B (for which you pay monthly premiums) when you were first eligible because you’re covered under a group health plan based on current employment, you can sign up for Part A and/or Part B Usually, you don’t pay a late enrollment penalty if you sign up during a Special Enrollment Period. This Special Enrollment Period doesn’t apply to people with End‑Stage Renal Disease (ESRD). You may also qualify for a Special Enrollment Period if you’re a volunteer serving in a foreign country.

Medicare Supplement Open Enrollment Period

You have a 6-month Medigap (Medicare Supplement Insurance) policy open enrollment period which starts the first month you’re both 65 and enrolled in Part B. This period gives you a guaranteed right to buy any Medicare Supplement policy sold in your state. Once this period starts, it can’t be delayed or replaced.

How Much Does Part A Coverage Cost?

You usually don’t pay a monthly premium for Part A coverage if you or your spouse paid Medicare taxes while working. If you aren’t eligible for premium-free Part A, you may be able to buy Part A if you meet one of the following conditions:

You’re 65 or older, and you’re entitled to (or enrolling in) Part B and meet the citizenship and residency requirements.

You’re under 65, disabled, and your premium-free Part A coverage ended because you returned to work. If you’re under 65 and disabled, you can continue to get premium-free Part A for up to 8.5 years after you return to work.)

How Much Does Part B Coverage Cost?

You pay the Part B premium each month. Most people will pay the standard premium amount. However, if your modified adjusted gross income as reported on your IRS tax return from 2 years ago (the most recent tax return information provided to Social Security by the IRS) is above a certain amount, you may pay more.

Your modified adjusted gross income is your adjusted gross income plus your tax exempt interest income. Each year, Social Security will notify you if you have to pay more than the standard premium. Whether you pay the standard premium or a higher premium can change each year depending on your income. If you have to pay a higher amount for your Part B premium and you disagree (even if you get RRB benefits), call Social Security at 1-800-772-1213. TTY users should call 1-800-325-0778. You can also view the fact sheet “Medicare Part B Premiums: Rules For Beneficiaries With Higher Incomes” by visiting www.socialsecurity.gov/pubs/10536.pdf.

A "Medicare Supplement policy" (also referred to as a “Medigap policy”) is private health insurance that is designed to supplement Original Medicare. This means it helps pay some of the health care costs (“gaps”) that Original Medicare doesn’t cover (like copayments, coinsurance, and deductibles). If you have Original Medicare and a Medicare Supplement policy, Medicare will pay its share of the Medicare-approved amounts for covered health care costs. Then your Medicare Supplement policy pays its share. A Medicare Supplement policy is different from a Medicare Advantage Plan (like an HMO or PPO) because those plans are ways to get Medicare benefits, while a Medicare Supplement policy only supplements your Original Medicare benefits. Note: Medicare doesn’t pay any of the costs for you to get a Medicare Supplmenet policy.

In some states, you may be able to buy another type of Medicare Supplement policy called Medicare SELECT. SELECT plans are standardized plans that may require you to see certain providers and may cost less than other Medicare Supplement plans.

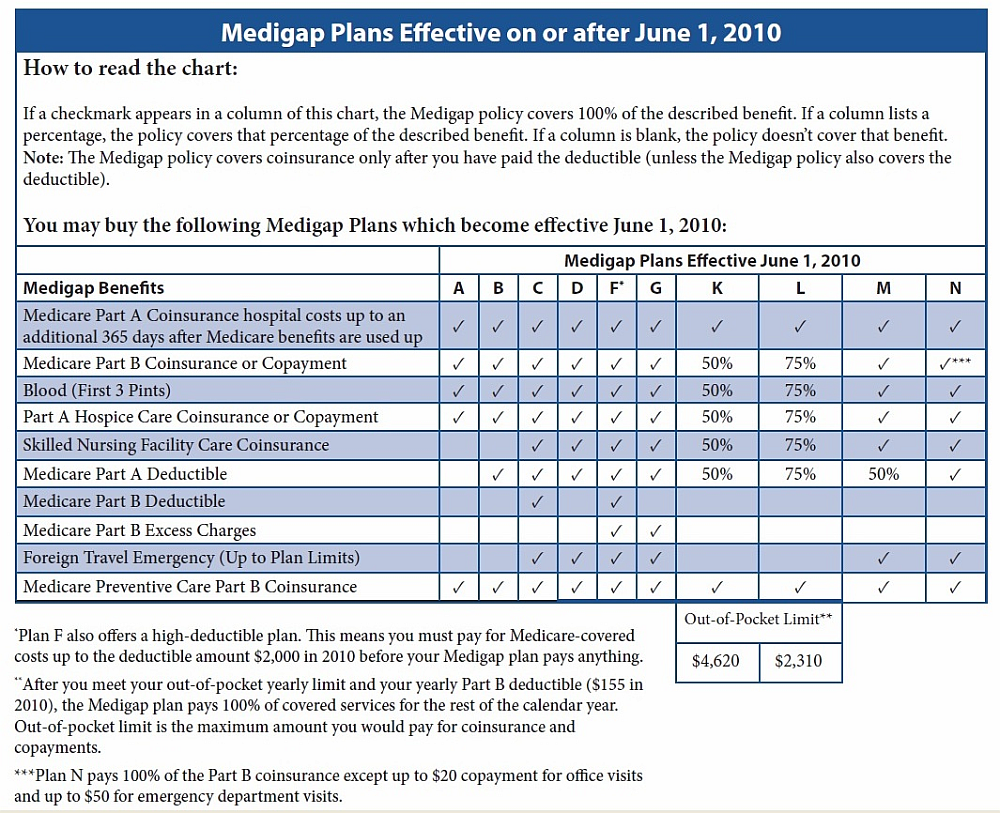

Medigap Plans Effective after June 1, 2010

Every Medicare Supplement policy must follow Federal and state laws designed to protect you, and the policy must be clearly identified as “Medicare Supplement Insurance.” Medicare Supplement insurance companies in most states can only sell you a “standardized” Medicare Supplement policy identified by letters A through N. (See Chart to the Left) Each standardized Medicare Supplement policy must offer the same basic benefits, no matter which insurance company sells it. Cost is usually the only difference between Medicare Supplement policies with the same letter sold by different insurance companies.

What types of Medicare Supplement policies can insurance companies sell?

Medicare Supplement insurance companies can sell you only a “standardized” Medicare Supplement policy. All Medicare Supplement policies must have specific benefits so you can compare them easily. (See Chart Above) In most cases, an insurance company must sell you a Medicare Supplement policy, even if you have health problems. Listed below are certain times that you’re guaranteed the right to buy a Medicare Supplement policy:

When you’re in your Medicare Supplement open enrollment period.

If you have a guaranteed issue right.

You may also buy a Medicare Supplement policy at other times, but the insurance company can deny you a Medicare Supplement policy based on your health.

Comparing Medicare Supplement costs

As discussed above, the cost of Medicare Supplement policies can vary widely. There can be big differences in the premiums that different insurance companies charge for exactly the same coverage. As you shop for a Medicare Supplement policy, be sure to compare the same standardized plan of Medicare Supplmenet policy, and consider the mode of pricing used. For example, compare a Medicare Supplement Plan F from one insurance company with a Medicare Supplement Plan F from another insurance company.

The cost of your Medicare Supplement policy may also depend on whether the insurance company does any of the following:

Offers discounts (such as discounts for women, non-smokers, or people who are married; discounts for paying annually; discounts for paying your premiums using electronic funds transfer; or discounts for multiple policies).

Uses medical underwriting, or applies a different premium when you don’t have a guaranteed issue right, or aren’t in a Medigap Open Enrollment period.

Sells Medicare SELECT policies that may require you to use certain providers. If you buy this type of Medigap policy, your premium may be less.

Offers a “high-deductible option” for Medicare Supplement Plan F. If you buy Medicare Supplement Plan F with a high-deductible option, you must pay the first $2,000 (in 2011) of deductibles, copayments, and coinsurance not paid by Medicare before the Medicare Supplement policy pays anything. You must also pay a separate deductible ($250 per year) for foreign travel emergency services

"Medicare & You" and "Choosing a Medigap Policy"

The information referenced above was hand selected from the most pertinent infomation included in the "Choosing a Medigap Policy" A Guide to Health Insurance for People with Medicare, and "2011 Medicare & You Handbook" A Guide to everything about Medicare. Please click the thumbnails to the left and take time to review the infomation in each Guide Book. While reviewing the infomation if you have any questions feel free to give Senior Market Supplements a call at 402- 467-0008 or use our "Contact" Page

Medicare Basics

Medicare Basics